Navigating the mortgage application timeline explained can feel overwhelming, but understanding each step makes it easier. From pre-approval to closing, we break down the entire process in simple terms to help you secure your dream home faster and with less stress.

Mortgage Application Timeline Explained: The Big Picture

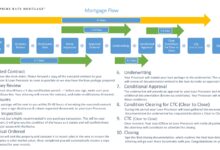

Understanding the full mortgage application timeline explained is crucial for any homebuyer. It’s not just about filling out forms—it’s a journey that involves preparation, documentation, communication, and patience. On average, the entire process takes between 30 to 45 days, though it can vary based on loan type, lender efficiency, and individual circumstances.

According to the Mortgage Bankers Association (MBA), the average mortgage closing time in 2023 was 44 days. This includes everything from application submission to final funding. But why does it take so long? Each phase has specific requirements, verifications, and legal checks that ensure both borrower and lender are protected.

Why the Timeline Matters

Knowing the mortgage application timeline explained helps you plan better. Whether you’re buying a new home or refinancing, timing affects your move-in date, interest rates, and even your negotiating power with sellers. A delayed loan can cost you a house, especially in competitive markets.

- Delays can cause you to miss out on a home.

- Understanding the timeline reduces stress and surprises.

- It allows you to coordinate with real estate agents and movers efficiently.

Factors That Influence the Duration

Several variables impact how long your mortgage application takes. These include credit score, down payment size, property type, and whether you’re purchasing or refinancing. Lenders also differ in processing speed—some offer ‘express’ services, while others may take weeks just to review documents.

“The key to a smooth mortgage process is preparation. The more organized you are upfront, the faster you’ll close,” says Sarah Johnson, a senior loan officer at Fairway Independent Mortgage.

Step 1: Pre-Qualification – The First Glimpse

Before diving into the mortgage application timeline explained, you start with pre-qualification. This initial step gives you an estimate of how much you might be able to borrow. It’s typically quick—often completed in under an hour—and requires basic financial information like income, debts, and assets.

Pre-qualification is not a guarantee. It’s a soft check, meaning lenders don’t pull your credit report yet. Instead, they use self-reported data to give you a ballpark figure. This number helps you set realistic expectations when house hunting.

What Information Do You Need?

To get pre-qualified, you’ll need to provide:

- Monthly income (pay stubs or tax returns)

- Current debts (credit cards, car loans, student loans)

- Estimated down payment amount

- Credit score range (if known)

While this step is informal, being honest and accurate ensures you don’t fall in love with a home you can’t afford.

How Long Does Pre-Qualification Take?

Most lenders complete pre-qualification within 24 hours. Some online platforms even offer instant estimates. However, this is not the same as pre-approval, which carries more weight with sellers.

For example, Zillow’s mortgage calculator allows users to input their financial details and receive an estimated loan amount in minutes. But remember: this is just a starting point.

Mortgage Application Timeline Explained: Step 2 – Pre-Approval

Pre-approval is where the mortgage application timeline explained becomes more serious. This step involves a hard credit check and verification of your financial documents. Once approved, you’ll receive a pre-approval letter stating the loan amount you qualify for.

This letter is powerful. In competitive housing markets, sellers often require pre-approval letters before accepting offers. It shows you’re a serious buyer with financing lined up.

Documents Required for Pre-Approval

To move forward, lenders will ask for:

- Two recent pay stubs

- W-2 forms from the past two years

- Bank and investment account statements

- Tax returns (if self-employed)

- Photo ID and Social Security number

Providing complete and accurate documentation speeds up the process. Missing or inconsistent information can delay your application by days or even weeks.

mortgage application timeline explained – Mortgage application timeline explained menjadi aspek penting yang dibahas di sini.

How Long Does Pre-Approval Take?

Typically, pre-approval takes 1 to 3 business days. Some lenders offer same-day approval if all documents are submitted promptly. The result is a conditional commitment—meaning you’re approved pending final underwriting and property appraisal.

“A strong pre-approval letter can make or break your offer in a bidding war,” notes real estate agent Mark Thompson from Redfin.

Step 3: House Hunting with Confidence

Now that you’re pre-approved, you can shop for homes within your budget. This phase isn’t part of the official mortgage application timeline explained, but it sets the stage for everything that follows.

Working with a real estate agent who understands your financing situation can help you target homes that match your loan eligibility. You’ll also learn about local market conditions, such as average days on market and price trends.

Setting Your Budget Realistically

Just because you’re approved for $500,000 doesn’t mean you should spend that much. Consider other costs like property taxes, insurance, maintenance, and HOA fees. A good rule of thumb is to keep your total housing expenses below 28% of your gross monthly income.

- Use online tools like Bankrate’s affordability calculator to fine-tune your budget.

- Factor in future expenses like renovations or family growth.

- Leave room for emergencies—don’t stretch your budget to the limit.

Why Pre-Approval Strengthens Your Offer

In a seller’s market, multiple offers are common. A buyer with a pre-approval letter has a significant advantage over those who are only pre-qualified or haven’t started the mortgage process.

Sellers want assurance that the deal will close. A pre-approval letter demonstrates that a lender has already reviewed your finances and is ready to fund the loan—subject to appraisal and title clearance.

Mortgage Application Timeline Explained: Step 4 – Making an Offer and Going Under Contract

Once you find the right home, your agent helps you submit an offer. If accepted, you enter into a purchase agreement and the home goes “under contract.” This is a critical milestone in the mortgage application timeline explained.

At this point, you’ll typically pay an earnest money deposit—usually 1% to 3% of the purchase price—to show your commitment. This money is held in escrow and applied to your down payment at closing.

What Happens After the Offer Is Accepted?

After going under contract, you officially begin the formal mortgage application process. You’ll work with your lender to complete the Uniform Residential Loan Application (Form 1003), which collects detailed information about your income, assets, employment, and the property.

This form is standardized across the industry and used by Fannie Mae and Freddie Mac. Completing it accurately is essential—errors can trigger delays later in underwriting.

Locking in Your Interest Rate

Now is the time to consider locking your interest rate. Rates can fluctuate daily, and a rate lock guarantees your rate for a set period (usually 30 to 60 days). If rates rise during that time, you’re protected.

However, if rates drop, you may not benefit unless you paid for a “float-down” option. Most experts recommend locking in once your offer is accepted and the home is under contract.

“Rate locks are a safety net. In volatile markets, they can save thousands over the life of the loan,” says financial advisor Lisa Chen.

Step 5: The Processing Phase – Gathering the Paperwork

Processing is where the mortgage application timeline explained gets detailed. A loan processor collects, organizes, and verifies all the documents needed for underwriting. This includes bank statements, tax returns, employment verification, and more.

It’s common for lenders to request additional documents during this phase—known as “conditions” or “APs” (additional provider documents). Responding quickly keeps the process moving.

Common Documents Requested During Processing

Lenders need to verify every aspect of your financial life. Expect requests for:

mortgage application timeline explained – Mortgage application timeline explained menjadi aspek penting yang dibahas di sini.

- Gift letters (if using gifted funds for down payment)

- Explanation letters for large deposits or credit inquiries

- Proof of homeowners insurance

- HOA documents (for condos or planned communities)

- Self-employment profit and loss statements

Each document must be clear, legible, and up to date. Blurry scans or incomplete forms can slow things down.

How Long Does Processing Take?

Processing typically lasts 7 to 10 days, depending on how fast you respond to requests. Some lenders use automated systems to speed up verification, while others rely on manual review.

For example, Rocket Mortgage uses AI-driven processing to reduce turnaround time, often completing this phase in under a week.

Mortgage Application Timeline Explained: Step 6 – Underwriting – The Decision Engine

Underwriting is the heart of the mortgage application timeline explained. This is where a licensed underwriter evaluates your risk as a borrower and decides whether to approve, suspend, or deny your loan.

The underwriter reviews your credit history, debt-to-income ratio (DTI), loan-to-value ratio (LTV), employment stability, and the property’s value. They also ensure the loan meets agency guidelines (Fannie Mae, FHA, VA, etc.).

What Underwriters Look For

Key factors in the underwriting decision include:

- Credit score (typically 620+ for conventional loans)

- Debt-to-income ratio (preferably below 43%)

- Down payment size (20% avoids PMI on conventional loans)

- Reserves (some lenders require 2–6 months of mortgage payments in savings)

- Property condition and appraisal results

If any red flags appear—like a recent job change or a drop in credit score—the underwriter may request clarification.

Possible Underwriting Outcomes

There are four main outcomes:

- Approval: Your loan is cleared to close.

- Approval with Conditions: You must provide additional documents or meet specific requirements.

- Suspension: The process stops until missing info is provided.

- Denial: The loan is rejected, often due to high risk.

Most applications receive conditional approval. Don’t panic if you get a list of conditions—it’s a normal part of the process.

“Underwriting isn’t meant to trip you up. It’s there to protect everyone involved in the transaction,” explains mortgage underwriter James Reed.

Step 7: Appraisal and Home Inspection – Two Different Things

During the mortgage application timeline explained, two critical evaluations occur: the appraisal and the home inspection. While often confused, they serve very different purposes.

The appraisal is ordered by the lender to determine the property’s market value. The home inspection is for your benefit, revealing potential issues with the home’s structure, systems, and safety.

How the Appraisal Works

A licensed appraiser visits the property and compares it to similar homes recently sold in the area (comps). If the appraisal comes in lower than the purchase price, it can cause problems.

For example, if you’re buying a home for $400,000 but it appraises at $380,000, the lender may only finance 80% of $380,000 ($304,000), leaving you to cover the $20,000 gap—or renegotiate the price.

According to the Appraisal Foundation, appraisal delays were a top reason for closing delays in 2022.

Why a Home Inspection Is Crucial

Even if the appraisal is fine, a home inspection can uncover hidden issues like mold, foundation cracks, or outdated electrical systems. You can use the inspection report to negotiate repairs or credits with the seller.

mortgage application timeline explained – Mortgage application timeline explained menjadi aspek penting yang dibahas di sini.

- Always hire a certified inspector.

- Be present during the inspection to ask questions.

- Review the report carefully before deciding on next steps.

Skipping this step could lead to costly surprises after you move in.

Mortgage Application Timeline Explained: Step 8 – Final Loan Approval and Closing Disclosure

Once underwriting is complete and all conditions are satisfied, you’ll receive final loan approval. This means the lender is ready to fund your loan, pending closing.

About three days before closing, you’ll receive the Closing Disclosure (CD), a five-page document that details your loan terms, monthly payments, fees, and closing costs. Compare it carefully to your Loan Estimate (LE), which you received within three days of applying.

Key Elements of the Closing Disclosure

The CD includes:

- Loan amount and interest rate

- Monthly principal and interest payment

- Estimated taxes and insurance

- Origination fees and lender charges

- Prepaid items (escrow, interest, etc.)

By law, the numbers on the CD must be substantially similar to the LE. If there are major changes, you have the right to ask questions or delay closing.

What to Do If You Spot Errors

If you notice discrepancies—like a higher interest rate or unexpected fees—contact your lender immediately. You have a three-day review period to raise concerns.

The Consumer Financial Protection Bureau (CFPB) requires lenders to provide accurate disclosures to protect borrowers from unfair practices.

“The Closing Disclosure is your final chance to verify everything. Don’t sign anything until you understand every line item,” warns consumer advocate Elena Martinez.

Step 9: The Closing Day – Signing the Papers

Closing day is the final step in the mortgage application timeline explained. You’ll meet with your lender, real estate agent, and possibly a title officer to sign a stack of documents.

The process usually takes 1 to 2 hours. You’ll need to bring a government-issued ID and a certified check or wire transfer for your closing costs and down payment (if not already paid).

Documents You’ll Sign

Key documents include:

- Mortgage Note: Your promise to repay the loan.

- Mortgage or Deed of Trust: Secures the loan against the property.

- Closing Disclosure: Final confirmation of terms.

- Truth-in-Lending Act (TILA) Disclosure: Summarizes loan costs.

- Warranty Deed: Transfers ownership from seller to you.

Take your time reading each document. Ask questions if anything is unclear.

When Do You Get the Keys?

In most cases, you’ll receive the keys immediately after signing, once the lender wires the funds to the seller. However, in some states, funding can take 1–2 business days, delaying key handover.

Coordinate with your real estate agent to confirm the exact timing.

Mortgage Application Timeline Explained: Step 10 – Post-Closing and First Payment

After closing, your lender will record the deed and mortgage with the local county. You’ll receive a final package confirming ownership and loan details.

Your first mortgage payment is typically due one month after closing. For example, if you close on March 15, your first payment is due May 1 (April’s payment is collected at closing as prepaid interest).

mortgage application timeline explained – Mortgage application timeline explained menjadi aspek penting yang dibahas di sini.

Setting Up Auto-Pay and Escrow

Most lenders offer auto-pay options to avoid late payments. You can also set up an escrow account to pay property taxes and insurance automatically each month.

- Auto-pay often comes with a small interest rate reduction (0.125%).

- Escrow accounts simplify budgeting for annual bills.

- Monitor your escrow balance annually to avoid shortages.

What Happens If You Miss a Payment?

If you miss a payment, you’ll likely incur a late fee. After 15–30 days, it may be reported to credit bureaus, hurting your credit score. After 90+ days, foreclosure proceedings could begin.

If you’re struggling, contact your lender immediately. Many offer forbearance or repayment plans.

“Communication is key. Lenders would rather work with you than go through foreclosure,” says HUD housing counselor David Kim.

How long does the entire mortgage application timeline explained take?

The average mortgage application timeline explained takes 30 to 45 days from application to closing. Pre-approval can happen in 1–3 days, while underwriting and appraisal typically take 10–14 days. Delays often stem from incomplete documentation, slow appraisals, or title issues.

Can I speed up the mortgage application timeline explained?

Yes. You can accelerate the process by submitting complete and accurate documents early, responding quickly to lender requests, choosing a fast lender, and locking your rate promptly. Working with an experienced real estate agent and mortgage broker also helps streamline coordination.

What causes delays in the mortgage application timeline explained?

Common delays include missing paperwork, low appraisals, underwriting conditions, title problems, and slow responses from buyers or sellers. Self-employed borrowers may face longer verification times. Choosing a lender with strong processing systems can reduce these risks.

Is pre-approval the same as final approval?

No. Pre-approval is conditional and based on preliminary information. Final approval comes after underwriting, appraisal, and verification of all documents. Many borrowers get pre-approved but fail to get final approval due to changes in financial status or property issues.

What should I do if my mortgage is denied during the application timeline?

If denied, ask the lender for a detailed explanation. Common reasons include low credit score, high DTI, or insufficient income. You can reapply after improving your finances, appeal the decision, or explore alternative loan programs like FHA or USDA.

Understanding the mortgage application timeline explained empowers you to navigate the homebuying process with confidence. From pre-qualification to closing, each step builds toward homeownership. By staying organized, responsive, and informed, you can minimize delays and secure your new home efficiently. Remember, knowledge is power—especially when it comes to your biggest financial decision.

mortgage application timeline explained – Mortgage application timeline explained menjadi aspek penting yang dibahas di sini.

Further Reading: