Navigating the world of home financing? This online mortgage loan application guide reveals 7 powerful steps to help you secure your dream home loan—fast, easy, and stress-free.

Understanding the Online Mortgage Loan Application Guide

The digital transformation of the mortgage industry has made it easier than ever to apply for a home loan from the comfort of your home. An online mortgage loan application guide serves as your roadmap, simplifying what was once a complex and time-consuming process. With just a few clicks, you can compare lenders, check rates, and submit your application—all without stepping into a bank.

What Is an Online Mortgage Loan?

An online mortgage loan is a home financing solution where the entire borrowing process—from pre-approval to closing—is conducted via digital platforms. Unlike traditional methods that require in-person meetings and stacks of paperwork, online mortgages leverage secure technology to streamline every step.

- Lenders use encrypted portals to protect your personal and financial data.

- Applicants upload documents digitally instead of mailing or faxing them.

- Real-time tracking allows borrowers to monitor their application status 24/7.

According to the Consumer Financial Protection Bureau (CFPB), online mortgage applications have surged in popularity due to their convenience and transparency.

Why Use This Online Mortgage Loan Application Guide?

This comprehensive online mortgage loan application guide is designed to eliminate confusion and empower borrowers with knowledge. Whether you’re a first-time homebuyer or refinancing an existing property, understanding the digital mortgage landscape is crucial.

- It breaks down complex jargon into plain English.

- It outlines best practices for avoiding common pitfalls.

- It provides actionable checklists and timelines.

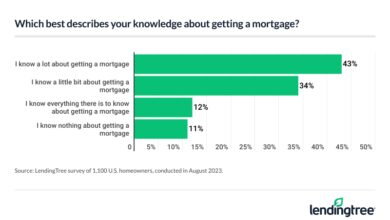

“The average homebuyer spends over 10 hours researching mortgage options before applying. A structured guide cuts that time in half.” — National Association of Realtors (NAR)

Step 1: Assess Your Financial Readiness

Before diving into the online mortgage loan application guide, take stock of your financial health. Lenders evaluate several key factors, including credit score, debt-to-income ratio, and available down payment. Being financially prepared not only increases your approval odds but also helps you secure better interest rates.

Check Your Credit Score

Your credit score is one of the most critical components of your mortgage application. Most lenders require a minimum FICO score of 620 for conventional loans, though government-backed loans like FHA may accept scores as low as 580.

- Obtain your free credit report from AnnualCreditReport.com, the only federally authorized site.

- Review for errors or discrepancies that could negatively impact your score.

- Dispute inaccuracies through the credit bureau’s official process.

Improving your score by even 20–30 points can save you thousands over the life of your loan. Pay down high balances, avoid new credit inquiries, and make all payments on time.

Calculate Your Debt-to-Income Ratio (DTI)

Your DTI ratio measures how much of your monthly income goes toward paying debts. Lenders typically prefer a DTI below 43%, although some programs allow higher ratios with compensating factors.

- Add up all monthly debt obligations: credit cards, car loans, student loans, alimony, etc.

- Divide the total by your gross monthly income (before taxes).

- Multiply by 100 to get your DTI percentage.

For example, if your monthly debts total $2,500 and your gross income is $7,000, your DTI is 35.7%. This falls well within acceptable limits for most lenders.

online mortgage loan application guide – Online mortgage loan application guide menjadi aspek penting yang dibahas di sini.

Step 2: Research and Compare Lenders

Not all lenders are created equal. One of the most valuable insights from this online mortgage loan application guide is learning how to choose the right lender for your needs. The digital marketplace offers a wide range of options—from big banks to fintech startups—each with unique advantages.

Types of Online Mortgage Lenders

Understanding the different types of lenders will help you make an informed decision. Here are the most common categories:

- Traditional Banks: Institutions like Chase or Bank of America offer online mortgage services but may have stricter qualification criteria.

- Credit Unions: Often provide competitive rates and personalized service, especially for members.

- Fintech Lenders: Companies like Rocket Mortgage or SoFi use AI-driven platforms to speed up approvals and reduce paperwork.

Each type has its pros and cons. Fintech lenders excel in speed and user experience, while traditional banks may offer more in-person support.

How to Compare Rates and Terms

When using this online mortgage loan application guide, always compare multiple loan estimates. The Loan Estimate form, mandated by the CFPB, provides a standardized breakdown of costs, interest rates, and terms.

- Look beyond the interest rate—examine origination fees, discount points, and closing costs.

- Use online comparison tools like NerdWallet or Bankrate to evaluate offers side by side.

- Check customer reviews on Trustpilot or the Better Business Bureau (BBB).

“Borrowers who compare at least three lenders save an average of $1,500 in the first five years of their mortgage.” — CFPB Study, 2023

Step 3: Get Pre-Approved Online

Pre-approval is a game-changer in the homebuying process. It signals to sellers that you’re a serious buyer and strengthens your negotiating position. Thanks to this online mortgage loan application guide, you can complete pre-approval entirely online in as little as 24 hours.

What Is Mortgage Pre-Approval?

Pre-approval is a conditional commitment from a lender stating how much they’re willing to lend you based on a preliminary review of your finances. It’s more robust than pre-qualification, which is based on self-reported information.

- Pre-approval involves verifying income, assets, employment, and credit history.

- It results in a formal letter you can present to real estate agents and sellers.

- It typically remains valid for 60 to 90 days.

Having a pre-approval letter can give you an edge in competitive housing markets where multiple offers are common.

Documents Needed for Online Pre-Approval

To streamline your experience with the online mortgage loan application guide, gather these documents in advance:

- Government-issued ID (driver’s license or passport)

- Recent pay stubs (last 30 days)

- W-2 forms or tax returns (last two years)

- Bank and investment account statements (last two months)

- Proof of additional income (e.g., rental income, alimony)

Most online platforms allow you to upload these files directly through a secure portal. Some even integrate with financial apps like Plaid to auto-verify account balances.

Step 4: Submit Your Full Mortgage Application

Once you’ve found a home and signed a purchase agreement, it’s time to submit your full mortgage application. This stage is where the online mortgage loan application guide becomes your most valuable tool, ensuring you don’t miss critical steps or deadlines.

online mortgage loan application guide – Online mortgage loan application guide menjadi aspek penting yang dibahas di sini.

Filling Out the Uniform Residential Loan Application (Form 1003)

The Uniform Residential Loan Application, commonly known as Form 1003, is the standard mortgage application used across the U.S. It collects detailed information about your income, assets, liabilities, and the property you intend to purchase.

- Be honest and accurate—any discrepancies can delay or derail your loan.

- Double-check entries for employment history, monthly payments, and asset values.

- Many online lenders auto-fill parts of the form using data you’ve already submitted during pre-approval.

You can access a sample form through the Fannie Mae website to familiarize yourself with the layout before starting.

Uploading Supporting Documents Securely

Security is paramount when submitting sensitive financial documents online. Reputable lenders use end-to-end encryption and multi-factor authentication to protect your data.

- Ensure the lender’s website uses HTTPS (look for the padlock icon in the browser).

- Avoid public Wi-Fi when uploading documents; use a secure home or cellular network.

- Keep digital copies of everything you submit for your records.

If you’re unsure about a platform’s security, check for third-party certifications like TRUSTe or McAfee Secure.

Step 5: Navigate the Underwriting Process

After submission, your application enters the underwriting phase—the most critical stage in the mortgage journey. This part of the online mortgage loan application guide demystifies what happens behind the scenes and how you can support a smooth approval.

What Happens During Underwriting?

Underwriting is the process where the lender evaluates your risk as a borrower. An underwriter reviews your financial profile, verifies all documentation, and assesses the value of the property through an appraisal.

- The underwriter may request additional information, such as clarification on large deposits or gaps in employment.

- They also confirm that the loan meets agency guidelines (e.g., Fannie Mae, FHA, VA).

- This process typically takes 30 to 45 days but can be faster with digital lenders.

Staying responsive during this phase is crucial. Promptly answering requests can prevent unnecessary delays.

Common Underwriting Challenges and How to Overcome Them

Even well-prepared applicants can face hurdles. Here are some common issues and solutions:

- Low Credit Score: Consider a co-signer or explore government-backed loans with more flexible requirements.

- High DTI: Pay off small debts or defer student loans to improve your ratio.

- Insufficient Down Payment: Look into down payment assistance programs or gift funds from family.

The key is proactive communication. If you anticipate a challenge, disclose it early and work with your loan officer to find a solution.

Step 6: Complete the Home Appraisal and Inspection

While not part of the loan application itself, the appraisal and inspection are integral to the mortgage process. This section of the online mortgage loan application guide explains their importance and how they affect your loan approval.

online mortgage loan application guide – Online mortgage loan application guide menjadi aspek penting yang dibahas di sini.

Understanding the Mortgage Appraisal

The appraisal ensures the home’s value matches or exceeds the loan amount. It protects both the lender and the borrower from overpaying.

- A licensed appraiser visits the property to assess its condition, size, location, and comparable sales.

- If the appraisal comes in low, you may need to renegotiate the price or make up the difference in cash.

- You have the right to review the appraisal report and dispute errors.

According to the Appraisal Foundation, low appraisals occur in about 8% of transactions, often in fast-moving markets.

Scheduling a Professional Home Inspection

Unlike the appraisal, which focuses on value, a home inspection evaluates the property’s structural and mechanical condition.

- Hire a certified inspector through organizations like ASHI (American Society of Home Inspectors).

- Attend the inspection to ask questions and observe potential issues.

- Use the report to request repairs or credits from the seller.

While not required by lenders, skipping an inspection can lead to costly surprises after closing.

Step 7: Finalize and Close Your Loan

Closing is the final step in the online mortgage loan application guide. It’s when you sign the last documents, pay closing costs, and officially become a homeowner. While exciting, this stage requires careful attention to detail.

Reviewing the Closing Disclosure (CD)

Three days before closing, you’ll receive the Closing Disclosure, a five-page document that details your final loan terms and costs.

- Compare it to your initial Loan Estimate to ensure no major changes.

- Verify the interest rate, loan amount, monthly payment, and closing fees.

- Contact your lender immediately if you spot discrepancies.

The CFPB mandates this waiting period to give borrowers time to review and ask questions.

What to Expect on Closing Day

Closing can happen in person or electronically, depending on your lender and state laws.

- For e-closings, you’ll sign documents using a secure digital platform.

- For in-person closings, bring a government-issued ID and a cashier’s check for closing costs (if required).

- The entire process usually takes 1–2 hours.

Once all documents are signed and funds are transferred, the title company records the deed, and you receive the keys to your new home.

Benefits of Using an Online Mortgage Loan Application Guide

Following a structured online mortgage loan application guide offers numerous advantages over navigating the process alone. From time savings to increased transparency, digital tools are transforming the homebuying experience.

online mortgage loan application guide – Online mortgage loan application guide menjadi aspek penting yang dibahas di sini.

Speed and Convenience

One of the biggest benefits is speed. Traditional mortgage applications can take weeks, but online platforms often reduce processing time by 50% or more.

- Instant document uploads eliminate mailing delays.

- Automated underwriting systems can approve loans in as little as 24 hours.

- Real-time chat support provides immediate answers to your questions.

A study by Mortgage Bankers Association (MBA) found that digital mortgage applications closed 15 days faster on average than paper-based ones.

Greater Transparency and Control

Online platforms give borrowers unprecedented visibility into their loan status.

- Dashboards show exactly where your application stands.

- Notifications alert you to required actions or updates.

- You can track every document, approval, and milestone.

This level of control reduces anxiety and empowers informed decision-making.

Common Mistakes to Avoid in the Online Mortgage Process

Even with the best online mortgage loan application guide, mistakes can happen. Being aware of common pitfalls helps you stay on track and avoid costly errors.

Applying for New Credit During the Process

Opening a new credit card or car loan while your mortgage is under review can hurt your credit score and DTI ratio.

- Lenders may re-pull your credit before closing.

- Any significant change can trigger a re-evaluation or denial.

- Wait until after closing to make large purchases.

This is one of the most frequently overlooked warnings in any online mortgage loan application guide.

Not Reading the Fine Print

It’s easy to rush through digital forms, but skipping the details can lead to misunderstandings.

- Read all disclosures, especially those about adjustable rates or prepayment penalties.

- Ask questions if terms are unclear.

- Save digital copies of every signed document.

Knowledge is power—take the time to understand what you’re agreeing to.

Is an online mortgage application safe?

online mortgage loan application guide – Online mortgage loan application guide menjadi aspek penting yang dibahas di sini.

Yes, online mortgage applications are safe when conducted through reputable, secure lenders. Look for HTTPS encryption, two-factor authentication, and compliance with federal regulations like the Gramm-Leach-Bliley Act (GLBA). Avoid sharing sensitive information over email or unsecured networks.

How long does an online mortgage application take?

The entire process typically takes 30 to 45 days from application to closing. However, pre-approval can be completed in as little as 24 hours, and some fintech lenders offer closings in under 20 days.

Can I apply for a mortgage online with bad credit?

Yes, you can apply for a mortgage online even with bad credit. Lenders offer specialized programs like FHA loans (minimum 580 FICO) or VA loans (no minimum score) for borrowers with lower credit scores. However, you may face higher interest rates or stricter requirements.

Do I need a down payment for an online mortgage?

Most loans require a down payment, though the amount varies. Conventional loans typically require 3%–20%, FHA loans require 3.5% with a 580+ credit score, and VA and USDA loans may require no down payment at all.

What happens if my online mortgage application is denied?

If your application is denied, the lender must provide a written explanation under the Equal Credit Opportunity Act (ECOA). You can appeal the decision, improve your financial profile, or apply with a different lender. Review the reason carefully and address any issues before reapplying.

Securing a mortgage no longer requires endless paperwork and long waits at a bank. With this comprehensive online mortgage loan application guide, you now have the tools and knowledge to navigate the digital lending landscape with confidence. From assessing your finances to closing the deal, each step is designed to save time, reduce stress, and maximize your chances of approval. Whether you’re a first-time buyer or a seasoned homeowner, embracing the online mortgage process is a smart, efficient way to achieve your homeownership goals.

online mortgage loan application guide – Online mortgage loan application guide menjadi aspek penting yang dibahas di sini.

Further Reading: